Over the past two years, humanity has endured such intersecting crises as the COVID pandemic, intensifying impacts from climate change and heightened racial injustice. These phenomena have deepened existing inequities throughout society. Around the world, women have frequently been among the worst affected.

Investors and legislators have taken note, shifting the focus to a just recovery: one that addresses the stark inequalities around the world to promote innovation and enhance growth, which would benefit everyone.

Seeking a just recovery

There is a growing realization that we need to find better ways of doing things. A just recovery is one that considers the voices of those most affected and prioritizes positive outcomes for people and the planet. A just recovery addresses systemic issues and creates avenues for the public to push for policies that protect and improve. In short, it is a unique opportunity to reimagine our future.1

While first and foremost a health crisis, the economic fallout of COVID has been enormous, disrupting livelihoods everywhere. Because nearly 58% of women worldwide work in the informal economy,2 they have earned less, saved less and have been likelier to fall into poverty.

The good news is that we are now at a tipping-point. Today, women control 32% of global wealth3. 13% of new billionaires were women. What’s more, 75% of millennial women take the lead in financial decision.

In other words, women of wealth have a high stake and determination power in navigating a just recovery.

Gender-lens investing

We believe that a women-focused just recovery offers investors innovative potential investment opportunities. A growing number of sustainability-oriented investors seek to integrate a gender lens to their portfolios.

Typically, gender-lens investing promotes women’s leadership by investing in companies that have diversity at board and executive level. Gender-lens thematic investing is booming.

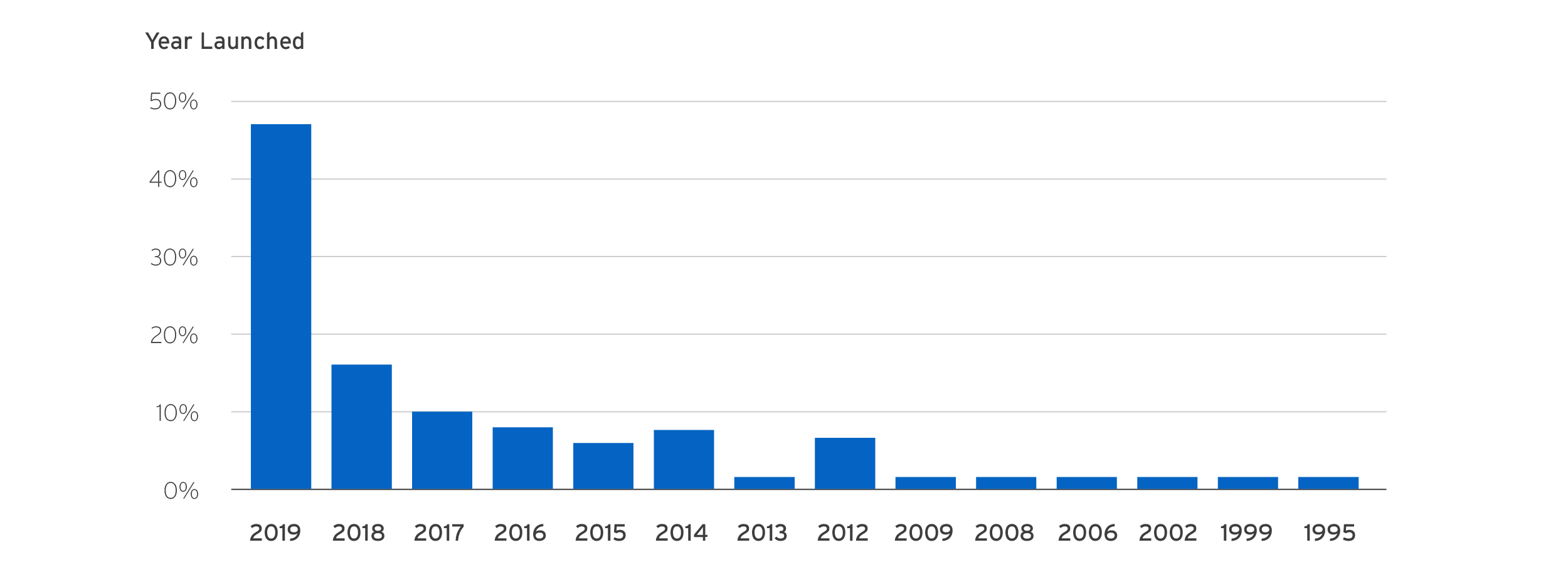

Project Sage 3.0 in 2020 includes 138 total funds deploying capital with a gender lens, up 58.6% from the 87 funds in 2019’s Project Sage 2.0, and up 138% from the 58 funds in 2017’s initial Project Sage report. Almost 50% of these funds launched in 2019. The rate of launch is increasing.4 (Figure 1)